Most people run into FOB terms when something goes wrong. A shipment shows up damaged. An invoice looks off. Accounting asks questions no one expected. That is when confusion hits.

FOB shipping point vs. FOB destination sounds simple on the surface, but the details matter more than most advice admits.

These terms decide who owns the goods, who carries risk, and when money and inventory show up on the books. Small misunderstandings create real problems.

I want to slow this down and walk you through it carefully. Not to memorize rules, but to understand why they work the way they do. Once that clicks, the rest gets easier.

What Does FOB Mean?

FOB stands for Free on Board. At its core, it answers one question. At what point does responsibility for the goods change hands?

That responsibility includes ownership, risk, and often shipping costs. FOB tells both sides when the seller’s job ends and the buyer’s job begins.

Historically, FOB came from maritime shipping. Goods were loaded onto ships, and the moment they crossed the ship’s rail mattered. That history still shapes the term, even though most shipments today move by truck, rail, or air.

In modern use, FOB is a contract term. It does not describe how goods move. It describes when legal and financial responsibility changes. That distinction is where most confusion starts.

What is FOB Shipping Point?

FOB shipping point means responsibility transfers at the seller’s location.

Once the goods are handed to the carrier, the buyer takes over. From that moment on, the buyer owns the goods, carries the risk, and usually pays for shipping.

Here is how that breaks down:

- Ownership transfer: Ownership passes to the buyer as soon as the goods leave the seller’s dock.

- Risk responsibility: If the goods are damaged or lost in transit, the buyer bears that risk.

- Shipping cost responsibility: The buyer pays freight charges, either directly or through reimbursement.

- Accounting impact: The seller records the sale when the goods ship. The buyer records inventory at the same time, even though the goods are still in transit.

A supplier ships equipment on Monday under FOB shipping point terms. The truck breaks down on Tuesday and damages the goods. Even though the buyer has not received anything yet, the loss belongs to the buyer. On paper and in practice, those goods were already theirs.

What is FOB Destination?

FOB destination pushes responsibility to the other end of the trip.

The seller keeps ownership and risk until the goods arrive at the buyer’s location. Only then does responsibility transfer.

Here is the same breakdown:

- Ownership transfer: Ownership moves to the buyer only after delivery is complete.

- Risk responsibility: The seller is responsible for loss or damage during transit.

- Shipping cost responsibility: The seller typically pays shipping costs, though this can vary by contract wording.

- Accounting impact: The seller records the sale upon delivery. The buyer records inventory at receipt, not shipment.

Using the same scenario as before, if goods ship on Monday under FOB destination terms and are damaged on Tuesday, the seller absorbs the loss. Until delivery happens, those goods still belong to them.

FOB Shipping Point vs. FOB Destination: Side-by-Side Comparison

The easiest way to understand the difference between FOB shipping point and FOB destination is to see how responsibility shifts at each stage of the shipment.

| Factor | FOB Shipping Point | FOB Destination |

|---|---|---|

| Ownership transfer | At shipment | At delivery |

| Risk of loss | Buyer during transit | Seller during transit |

| Freight payment | Usually buyer | Usually seller |

| Revenue recognition | At shipment | At delivery |

| Inventory recognition | Buyer records in transit | Buyer records upon receipt |

| Insurance responsibility | Buyer covers transit | Seller covers transit |

Once you know when ownership transfers, everything else falls into place. Risk, accounting, and insurance all follow that single handoff point.

How FOB Affects Accounting and Journal Entries

Accounting cares about FOB terms because timing matters. Revenue, inventory, and expenses all depend on when ownership changes. If that timing is wrong, the financial statements are wrong.

This is not about being picky. It is about matching reality to the books.

1. FOB Shipping Point Journal Entry Example

Under FOB shipping point, the sale happens when the goods ship.

The seller records revenue and removes inventory on the shipment date. The buyer records inventory and a payable at the same time.

Even though the goods are on a truck somewhere, they already belong to the buyer. Accounting reflects that reality.

2. FOB Destination Journal Entry Example

Under FOB destination, everything waits until delivery.

The seller keeps inventory on the books while goods are in transit. Revenue is recorded only after delivery. The buyer records inventory only when the goods arrive.

Until then, nothing has changed financially, even if the goods have been moving for days.

3. Inventory in Transit Explained

Inventory in transit causes a lot of stress because it feels intangible. But the rule is simple.

Inventory belongs on the books of whoever owns it at that moment.

Under shipping point terms, that is the buyer. Under destination terms, that is the seller. Physical location does not matter. Legal ownership does.

Who Should Use Which Option?

There is no universally better choice. The right option depends on priorities and risk tolerance.

When FOB Shipping Point Makes Sense

FOB shipping point often fits sellers who want clean handoffs.

It reduces liability exposure and simplifies responsibility. Buyers who have strong logistics teams or preferred carriers may also like the control it offers.

When FOB Destination Makes Sense

FOB destination appeals to buyers who want predictability.

They avoid transit risk and accounting complexity. Sellers sometimes use it to stay competitive or to keep tighter control over delivery quality.

Buyer vs. Seller Trade-Offs

FOB terms are about balance.

Sellers trade risk for simplicity. Buyers trade control for protection. Neither side is wrong. Problems arise only when expectations are unclear or mismatched.

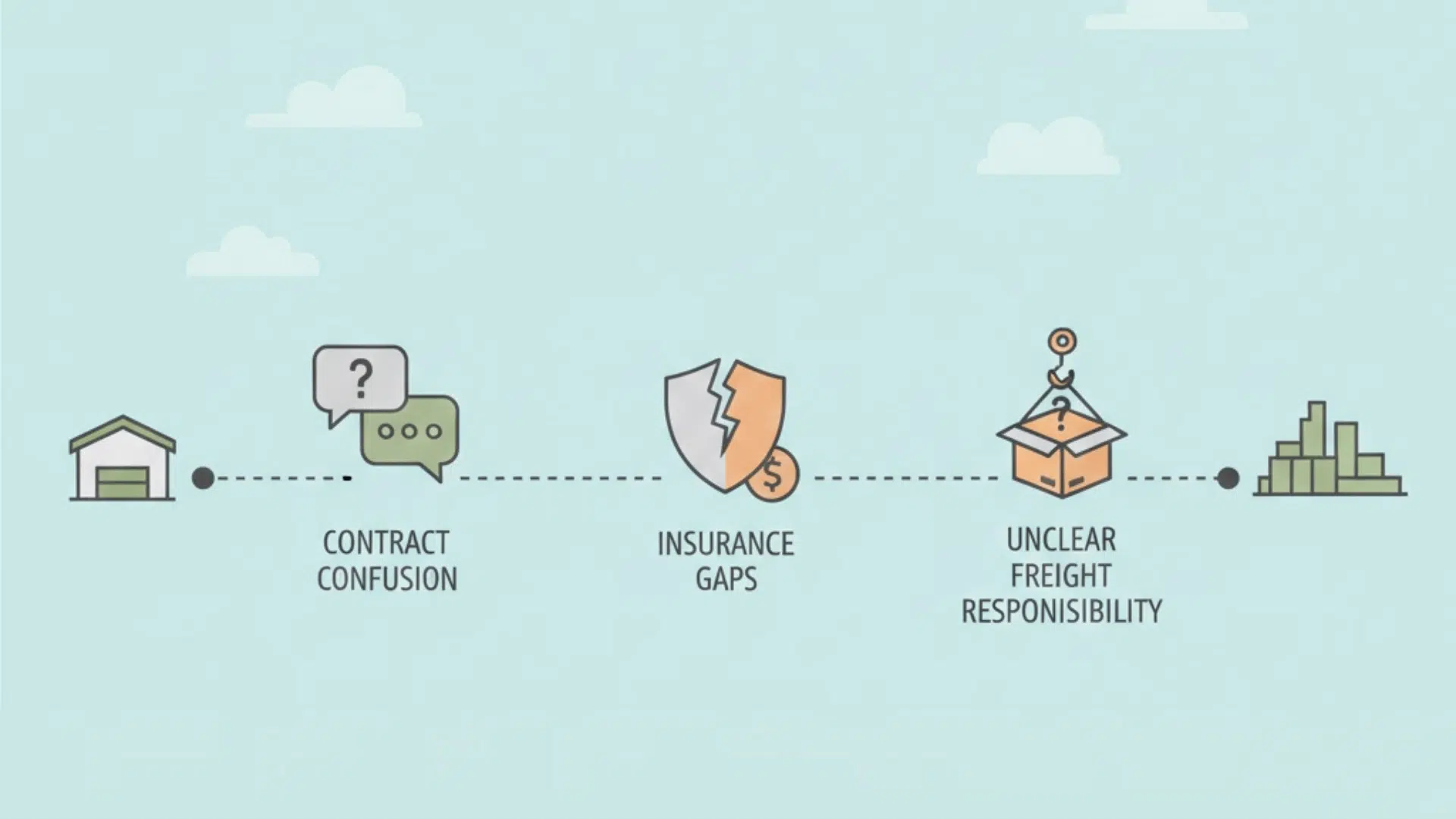

Risks and Common Mistakes with FOB Terms

Most issues do not come from bad intent. They come from assumptions. Common mistakes include:

- Assuming FOB means shipping is free: FOB has nothing to do with price discounts. It defines responsibility, not generosity.

- Confusing FOB with Incoterms: FOB is often used loosely, but it has specific meaning that does not always align with global trade rules.

- Not clarifying freight prepaid vs. collect: FOB alone does not fully explain who pays upfront versus who reimburses later.

- Insurance gaps during transit: If no one confirms who insures the goods, losses can turn into disputes fast.

Each mistake traces back to vague language. Clear contracts prevent almost all of them.

FOB vs. Incoterms: Important Clarification

FOB is widely misused, especially in international trade.

Incoterms are global rules designed for cross-border shipping. FOB technically applies only to sea freight under those rules, yet people apply it to trucks and planes anyway.

That does not automatically invalidate contracts, but it creates confusion.

When Incoterms apply, use them clearly. When FOB is used domestically, define it precisely. Mixing the two without explanation invites disputes.

Wrapping Up

FOB terms are not technical trivia. They shape ownership, risk, and financial timing in real ways. Once you understand how responsibility shifts, the logic behind the rules becomes calm and predictable.

FOB shipping point vs. FOB destination is not about right or wrong. It is about choosing where responsibility changes hands and making sure everyone agrees on that moment.

This matters most for buyers, sellers, and anyone touching accounting or logistics.

If you are unsure, read the contract language slowly and ask where risk transfers. That one answer usually clears everything else up.

Frequently Asked Questions

Who pays under FOB shipping point?

Under FOB shipping point, the buyer pays the shipping costs and assumes all transit risk once the goods leave the seller’s location.

What is the journal entry difference?

With FOB shipping point, entries are recorded at shipment. With FOB destination, revenue and inventory are recorded only after delivery.

What are the risks of FOB shipping point?

The buyer is responsible for loss, damage, or delays during transit, even if the goods have not yet been received.

Is FOB destination better for buyers?

FOB destination is often better for buyers because it shifts transit risk to the seller and simplifies inventory and revenue timing.

Is inventory recorded under FOB shipping point while in transit?

Yes. Under FOB shipping point, the buyer records inventory as soon as the goods ship, even while they are still in transit.