FOB shipping point is one of those terms that sounds simple but keeps tripping people up. I’ve seen smart business owners, students, and even accountants get tangled in it.

The confusion usually comes from mixing up ownership, shipping costs, and responsibility. They are related, but they are not the same thing. Most explanations online rush through the basics and leave out the “why,” which is where clarity actually comes from.

This post slows everything down. I’ll walk you through what the term really means, how it works in real life, and why small details matter more than people think. Let’s start with the foundation.

What is FOB Shipping Point?

FOB stands for “Free On Board.” It’s a shipping term used to define when ownership and responsibility for goods move from the seller to the buyer.

With FOB shipping point, ownership transfers at the seller’s shipping location. That location might be a warehouse, factory, or loading dock. The key idea is that once the goods are handed to the carrier, they legally belong to the buyer.

You’ll also see this called FOB origin. These two terms mean the same thing. They both point to the same moment in time. The moment the goods leave the seller’s control.

This term does not describe how fast goods move or how they are packaged. It only defines responsibility and timing. That’s why it shows up in contracts, invoices, and accounting rules.

When Does Ownership Transfer?

Ownership transfers at the shipping point. Not when the goods arrive. Not when they are unloaded. Not when the buyer signs for them.

The exact moment is when the seller loads the goods onto the carrier. That could be a truck, ship, or plane. From that point forward, the goods legally belong to the buyer.

This matters because ownership drives everything else. It affects who records inventory. It affects when revenue is recognized. It affects who bears the risk if something goes wrong.

A simple timeline helps:

- The seller prepares the goods.

- The goods are loaded onto the carrier.

- Ownership transfers to the buyer.

- The goods travel in transit.

- The goods arrive at the buyer’s location.

Once you see that sequence, the rest of FOB shipping point starts to make sense.

Who Pays Shipping and Who Bears the Cost?

This is where most confusion lives. Paying for shipping and bearing the cost are not always the same thing. One party can pay the carrier, while the other party absorbs the expense in the end.

Under FOB shipping point, the buyer bears the shipping cost. That means shipping is part of what it costs the buyer to acquire the goods.

Sometimes the buyer pays the carrier directly. This is called freight collect.

Other times the seller pays the carrier upfront and bills the buyer later. This is called freight prepaid.

In both cases, the buyer still bears the cost. The method of payment does not change responsibility.

A common misunderstanding is thinking “prepaid” means the seller absorbs the cost. That’s not true unless the contract clearly says so.

Who is Responsible for Damage or Loss?

Responsibility follows ownership.

With FOB shipping point, the buyer assumes risk once the goods leave the seller’s location. If the goods are damaged in transit, that loss belongs to the buyer.

This is why insurance matters. Buyers often carry transit insurance to protect against damage or theft. Sellers usually do not insure goods once ownership transfers.

Here’s a simple example. A seller ships machinery under FOB shipping point. The truck is in an accident halfway to the buyer. The machinery is damaged. Even though the buyer has not received it yet, the loss belongs to the buyer.

That feels uncomfortable to many people at first. But it’s consistent once you focus on ownership timing.

FOB Shipping Point in Accounting

FOB terms matter in accounting because they define when transactions are recorded. Timing changes numbers. Numbers change decisions.

Buyer Accounting Treatment

The buyer records inventory when ownership transfers. Under FOB shipping point, that happens when the goods leave the seller.

Even if the goods are still in transit, they belong on the buyer’s books.

Shipping costs paid by the buyer are added to inventory. They are not expensed right away. They become part of the cost of the goods.

A simple journal entry looks like this:

- Debit Inventory

- Credit Accounts Payable or Cash

Shipping costs are added to inventory, not recorded as a separate expense at purchase.

Seller Accounting Treatment

The seller records revenue at the moment the goods leave their location, because that’s when ownership legally transfers.

At that same point, the inventory is removed from the seller’s books, even though the goods are still in transit.

A simple journal entry looks like this:

- Debit Accounts Receivable

- Credit Revenue

And separately:

- Debit Cost of Goods Sold

- Credit Inventory

The seller does not wait for delivery. Shipment is the trigger.

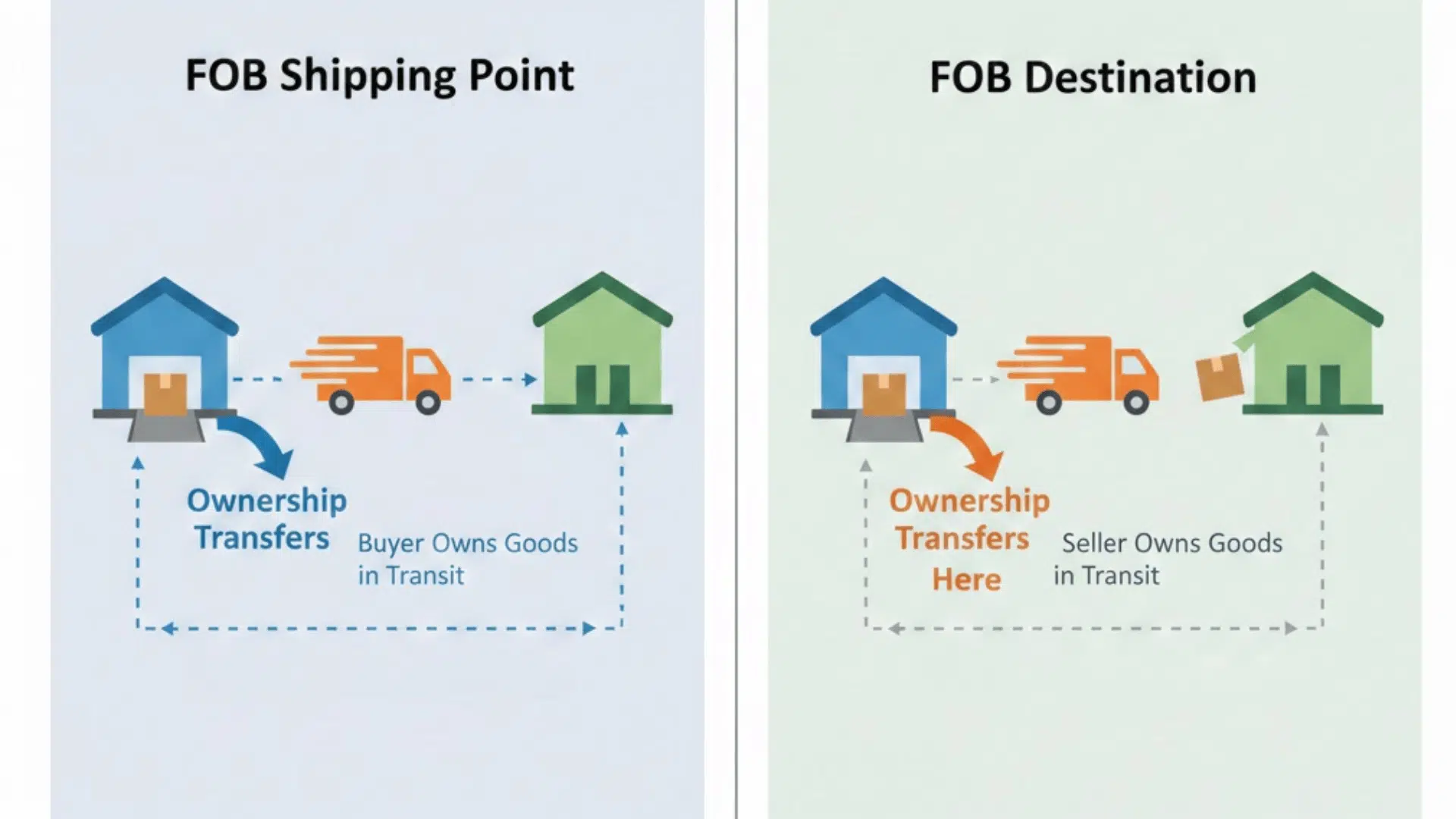

FOB Shipping Point vs. FOB Destination

FOB shipping point and FOB destination use the same logic, but they place the ownership handoff in different locations. That single change affects risk, accounting, and responsibility throughout the shipment.

FOB Shipping Point

With FOB shipping point, ownership transfers when goods leave the seller’s location. From that moment forward, the buyer owns the goods, records inventory, and carries transit risk, even though delivery has not happened yet.

FOB Destination

With FOB destination, ownership transfers only when goods arrive at the buyer’s location. Until delivery occurs, the seller retains ownership, records inventory, and remains responsible for goods in transit.

| Aspect | FOB Shipping Point | FOB Destination |

|---|---|---|

| Ownership transfer | At shipment | At delivery |

| Risk in transit | Buyer | Seller |

| Inventory timing | Buyer records at shipment | Buyer records at delivery |

| Revenue timing | Seller records at shipment | Seller records at delivery |

Once you understand one, the other becomes easy. The only thing that changes is the location where ownership flips.

FOB Shipping Point vs. CIF and Other Terms

Shipping terms start to feel less abstract once you see them side by side. While the details differ, most terms are really just different ways of answering the same ownership question.

| Term | Common Use | Who Handles Shipping | Insurance | Ownership Focus |

|---|---|---|---|---|

| FOB Shipping Point | Domestic shipping, North America | Buyer (cost-bearing) | Buyer | Transfers at origin |

| FOB Destination | Domestic shipping | Seller | Seller | Transfers at delivery |

| CIF | International trade | Seller | Seller | Transfers per contract |

| Other Incoterms | International trade | Varies by term | Varies by term | Defined per Incoterm |

FOB shipping point stays popular because it draws a clear line at the origin. CIF and other Incoterms are more detailed, especially for cross-border shipments, but they still revolve around the same idea.

How FOB Shipping Point Works in Real Situations

Imagine a furniture manufacturer shipping chairs to a retailer under FOB shipping point. The chairs are loaded onto a truck on Monday. At that moment, ownership transfers. The retailer records inventory on Monday, even though the chairs arrive on Wednesday.

Now look at an e-commerce setup. A wholesaler ships products to an online seller using FOB shipping point. Once the carrier picks up the boxes, the online seller owns the inventory. If the shipment is lost in transit, the loss belongs to the online seller, not the wholesaler.

In a damaged shipment scenario, the same rule applies. The buyer files the insurance claim because ownership transferred at shipment. From the seller’s perspective, the sale was already complete.

Once you lock onto the timing of ownership transfer, these outcomes stop feeling arbitrary and start feeling predictable.

Common Mistakes and Misconceptions

- Assuming the seller always pays shipping: Many people think prepaid freight means the seller absorbs the cost, when it often just means the seller pays upfront and bills the buyer later.

- Recording inventory only after delivery: Inventory is sometimes recorded when goods arrive, even though ownership transferred earlier, which leads to timing errors and misstatements in inventory and cost reporting.

- Recognizing revenue at receipt instead of shipment: Sellers often wait until delivery to record revenue, ignoring that under FOB shipping point, revenue should be recognized when goods leave the seller’s location.

- Confusing prepaid freight with seller-paid cost: Prepaid freight describes payment method, not responsibility, but it’s frequently mistaken as proof that the seller is bearing shipping costs.

- Ignoring FOB terms in invoices or contracts: FOB terms are often buried in paperwork and overlooked, causing teams to apply default assumptions instead of following the legally agreed ownership terms

Most of these mistakes happen because people focus on physical possession instead of legal ownership.

When Should Businesses Use FOB Shipping Point?

FOB shipping point works best when both sides are comfortable with how shipping and risk are handled.

| Perspective | Pros | Cons |

|---|---|---|

| Seller | Faster revenue recognition, less transit risk | Less control after shipment |

| Buyer | More control over carriers and insurance | Assumes transit risk |

For sellers, this term makes sense when the goal is a clean handoff. Once goods leave the dock, the sale is complete. There’s no responsibility tied to transit delays or damage.

For buyers, FOB shipping point fits when you already manage logistics well. You control carriers and insurance, but you also take on risk once the goods ship.

A simple checklist helps. Do you control shipping? Do you have transit insurance? Do you want ownership early? If yes, FOB shipping point is usually a good fit.

Wrapping Up

FOB shipping point is not complicated once you stop mixing concepts together.

Ownership, cost, and risk move in a specific order, and that order drives everything else. When you slow down and focus on timing, the accounting and logistics fall into place.

I’ve found that most confusion disappears once people stop asking who touches the goods and start asking who owns them at each step.

If you work with contracts or inventory, it’s worth reviewing your terms carefully. Take a look at your next invoice and notice exactly when ownership changes under FOB shipping point.

Frequently Asked Questions

What does FOB mean in shipping?

FOB stands for Free On Board. It defines the exact point at which ownership, risk, and responsibility for goods transfer from seller to buyer.

What is the difference between FOB and CIF?

FOB focuses on when ownership and risk transfer, while CIF includes cost, insurance, and freight, with the seller arranging and covering transport and insurance.

When is revenue recognized under FOB shipping point?

Revenue is recognized at shipment, when goods leave the seller’s location, because ownership and risk have already transferred to the buyer.